Most volatility indicators are reactive. VIX tells you what traders expect volatility to be. Realized vol tells you what it was. Both are looking backward or estimating forward based on current fear.

Gamma exposure is different. It tells you the mechanical conditions that will determine whether volatility expands or contracts – before it happens. It’s not a forecast based on sentiment. It’s a structural consequence of where options dealers are positioned right now.

Here’s how to use GEX to anticipate volatility regime changes before they hit your P&L.

The GEX-Volatility Connection

The link between gamma exposure and volatility is mechanical, not correlative. Here’s the chain:

Dealers hold a net gamma position based on the options they’ve sold and bought

That gamma position forces them to hedge by buying or selling the underlying as price moves

When net gamma is positive, dealer hedging counteracts price moves → volatility is suppressed

When net gamma is negative, dealer hedging amplifies price moves → volatility expands

This isn’t a pattern someone noticed in historical data. It’s math. Dealers are required to hedge their gamma positions. Their hedging mechanically affects realized volatility.

The signal to watch is not just the current Net GEX level – it’s the trend and position relative to the gamma flip.

Signal 1: Net GEX Declining Toward Zero

When Net GEX is positive but falling, the market is losing its volatility dampener. Dealers are holding less gamma, which means their stabilizing hedging flows are weakening. Volatility is likely to expand soon.

Watch for: Net GEX dropping from +$3B to +$1B over several days, even as price holds steady. That’s a setup for a vol expansion event.

Signal 2: Price Approaching the Gamma Flip

As price drifts toward the gamma flip level, the market is approaching the boundary between two volatility regimes. A cross of the gamma flip doesn’t always trigger instant volatility, but it raises the probability significantly.

When price crosses the gamma flip on a day with elevated options activity, expect vol to pick up within hours.

Once Net GEX turns negative, you’re in an amplifying regime. Realized volatility tends to exceed implied volatility in this environment – which means options buyers (especially puts) are being underpaid relative to what the market will actually deliver.

Trade implication: In negative gamma environments, long options tend to perform better than short premium strategies.

Signal 4: OpEx Gamma Expiration

Every options expiration removes gamma from the market. After a major OpEx – especially monthly or quarterly – the stabilizing gamma that was keeping volatility suppressed disappears. The following week often sees higher realized vol as the new options cycle builds.

Traders often ask how GEX compares to VIX. They measure different things:

GEX

VIX

What it measures

Dealer gamma positioning and hedging structure

Market’s expectation of 30-day S&P 500 volatility

Lead or lag?

Leading – structural conditions that will drive vol

Coincident/lagging – responds to what’s already happening

Driven by

Options positioning mechanics

Options implied volatility pricing

Best for

Anticipating vol regime changes

Measuring current fear/complacency

Updates

Continuously (real-time with live tools)

Continuously, but reflects current pricing not structure

The best approach uses both. GEX tells you the structural condition. VIX tells you the current market sentiment. When GEX turns negative and VIX is still low – that’s the setup where vol expansion is most likely and options are cheapest to buy.

The Vol Squeeze Setup: Trading GEX + VIX Together

One of the most powerful setups in options trading is the vol squeeze:

Conditions:

Net GEX is turning negative or already negative

VIX is low or declining (complacency)

Price is near or below the gamma flip

What it means: The structural conditions for vol expansion are in place, but the market hasn’t priced it yet. Options are cheap relative to what’s likely to be delivered.

The trade: Long puts or long straddles on SPY/SPX. The GEX structure is your reason to believe vol will expand. The low VIX is your reason the trade is cheap.

This isn’t a guaranteed setup. But the combination of negative gamma conditions + low implied volatility is historically one of the better asymmetric risk setups available to retail options traders.

How Gamma Exposure Explains Major Vol Events

Looking back at major volatility spikes – August 2024, early 2025 corrections, major macro events – a consistent pattern appears:

Markets had been trading in a high positive gamma environment (suppressed vol, grinding higher)

Net GEX began declining as options positioning shifted

Price drifted toward or through the gamma flip level

Once in negative gamma territory, small catalysts triggered outsized moves

Dealer hedging amplified the selling, creating the “cascade” effect

Traders watching GEX had advance warning that the structural conditions for a vol expansion were building – not because they predicted the catalyst, but because they could see the gamma environment shifting from stabilizing to destabilizing.

This is the edge GEX provides. Not prediction. Structural awareness.

Practical Checklist: Is a Vol Expansion Coming?

Use this before entering short premium positions (selling options):

[ ] Is Net GEX positive and stable? (Good for selling premium)

[ ] Is price well above the gamma flip? (Positive gamma cushion)

[ ] Has Net GEX been declining recently? (Weakening dampener – caution)

[ ] Is price within 1% of the gamma flip? (Vol expansion risk elevated)

[ ] Has Net GEX turned negative? (Do not sell premium without strong hedge)

[ ] Is there a major macro event this week (FOMC, CPI, OpEx)? (GEX structure may shift rapidly)

If any of the last three boxes are checked, reconsider your short premium sizing.

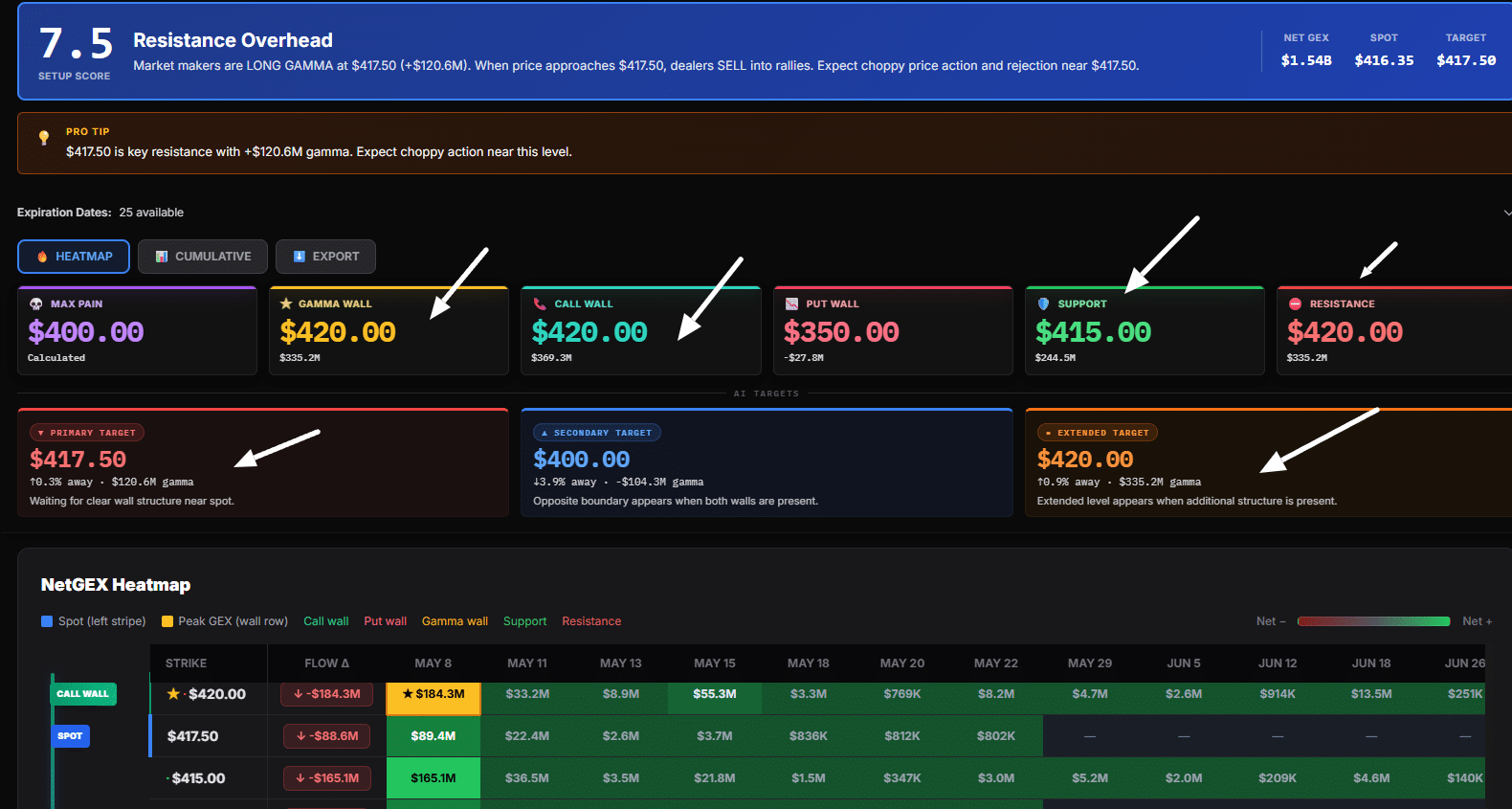

Net GEX in real time – you can see whether it’s positive, negative, and how the magnitude compares to recent sessions

Setup score – the AI factors GEX regime into its score, with lower scores indicating higher risk/volatility conditions

Plain-English regime description – “Market makers are SHORT GAMMA. Expect amplified volatility and trending conditions.”

Combined with the NetGEX heatmap showing where the gamma flip sits relative to price, you have everything you need to assess the vol environment before placing a trade.

ALT: SweepAlgo AI analysis dashboard showing setup score, Net GEX dollar figure, and plain-English gamma regime description indicating resistance overhead and dealer behavior for SPY

Gamma exposure is the most reliable leading indicator of volatility regime changes available to retail traders. Not because it predicts catalysts – it doesn’t – but because it defines the structural conditions that determine whether a catalyst will cause a small ripple or a large wave.

When dealers are long gamma, the market absorbs shocks. When dealers are short gamma, the market amplifies them. Knowing which condition is in place before you size your positions is the edge.