This guide explains exactly how options expiration works, what happens to your contracts, why price behaves differently in expiration week, and how GEX data (specifically max pain) gives you a structural edge when trading around it.

Every options contract has a hard deadline. When that deadline hits, one of three things happens: your option expires worthless, it’s exercised, or you’ve already closed it. Which outcome you get depends almost entirely on decisions you make before expiration – not on the day itself.

Table of Contents

- What Is Options Expiration?

- Types of Expiration: Weekly, Monthly, Quarterly

- What Happens to Your Option at Expiration

- How Theta Accelerates Into Expiration

- What Is Expiration Week and Why It Matters

- Max Pain: Price Gravity Around Expiration

- How to Manage Options Into Expiration

- 0DTE Options: Expiration as the Trade

- FAQ

What Is Options Expiration?

Options expiration is the date and time after which an options contract no longer exists. Once a contract expires, it either has value (and is settled) or it’s worthless – and you can no longer trade it.

For most U.S. equity options, expiration officially occurs on the expiration date at market close. The last day you can trade most equity options is the expiration Friday (or Monday/Wednesday for SPX).

Why expiration matters:

Expiration creates a hard boundary on your trade. Unlike stocks, which you can hold indefinitely, options have a built-in clock. The closer you get to expiration with an unprofitable position, the less time you have to recover – and the more theta (daily decay) is working against you.

Types of Expiration: Weekly, Monthly, Quarterly

Not all options expire on the same schedule. Here’s how the main types work:

| Type | Frequency | Expires | Common Use |

|---|---|---|---|

| Weekly (SPY/SPX) | Every Mon, Wed, Fri | End of that day | Short-term directional, 0DTE |

| Weekly (single stocks) | Every Friday | Market close Friday | Weekly trades, earnings plays |

| Monthly | 3rd Friday of the month | Market close | Standard expiration, most OI |

| Quarterly (LEAPS) | March, June, Sept, Dec | 3rd Friday of month | Long-term positions, hedges |

| LEAPS | 1–3 years out | Future Friday | Long-term directional or hedges |

Monthly expirations (the third Friday of each month) carry the largest open interest of any cycle. This is when institutional positioning is heaviest, which means GEX levels and max pain are most influential on price behavior.

SPX/SPY specifics: SPX options expire three times per week – Monday, Wednesday, and Friday. SPY follows the same schedule. The daily expiration structure is what enables 0DTE trading.

What Happens to Your Option at Expiration

There are three possible outcomes when your option reaches expiration:

1. Expires worthless (most common for OTM options)

If your option is out-of-the-money at expiration, it expires with zero value. You lose 100% of the premium you paid. Nothing else happens – you don’t owe anything, you don’t receive anything. The contract simply ceases to exist.

This is why buying deep OTM options close to expiration is so risky – the probability of this outcome is very high.

2. Exercised (in-the-money at expiration)

If your option is in-the-money at expiration, it will typically be auto-exercised by your broker. For a call, that means you’d buy 100 shares at the strike price. For a put, you’d sell 100 shares at the strike price.

For most retail traders, this is not what you want. Exercising means you need to fund the share purchase (for calls) or deliver shares (for puts). Most retail traders don’t have the capital or shares ready. The better move is almost always to sell the contract before expiration rather than exercise it.

Many brokers will automatically close ITM options contracts in the final hour of expiration day to prevent inadvertent exercise. Check your broker’s specific policy.

3. Closed before expiration (recommended for beginners)

The cleanest outcome: you sell your contract before expiration day. You capture whatever profit or limit whatever loss exists at that point, and you’re done. No exercise risk, no margin calls, no forced share purchases.

How Theta Accelerates Into Expiration

Theta is the daily cost of holding an options contract. It’s not linear – it accelerates significantly as expiration approaches.

A rough guide to how extrinsic value decays:

| Days to Expiration | Daily Theta Decay Rate |

|---|---|

| 60 DTE | Slow – roughly 1/60th of extrinsic value per day |

| 30 DTE | Moderate – roughly 1/30th per day |

| 14 DTE | Accelerating – noticeably faster |

| 7 DTE | Fast – substantial daily bleed |

| 2–3 DTE | Very fast – losing significant value each session |

| 0DTE | Maximum – all extrinsic value must disappear by close |

This is why the common advice is to buy options with at least 21–45 days to expiration as a beginner. Close to expiration, theta is eating your position whether the stock moves or not.

The flip side: if you’re selling options (covered calls, cash-secured puts), theta works in your favor. Selling options in the 30–45 DTE range and closing at 50% profit is a standard theta-capture strategy for that reason.

What Is Expiration Week and Why It Matters

Expiration week (sometimes called “OPEX week”) is the week leading up to the monthly options expiration – the third Friday of the month.

During expiration week, market behavior often shifts noticeably:

- Pinning behavior: Price tends to gravitate toward the strike with the most open interest (max pain) as dealers manage their expiring books

- Reduced volatility: Positive gamma from large open interest at specific strikes suppresses large directional moves

- Whipsaw action: As positions are closed, delta-hedging flows can cause sharp intraday reversals with no clear fundamental catalyst

For options buyers, expiration week is a high-risk environment. Theta is maximal, pinning behavior can trap your position, and any gap down or up can reverse rapidly as dealers adjust.

For options sellers, expiration week is often favorable – premium collapses rapidly and pins near max pain produce easy wins on short positions.

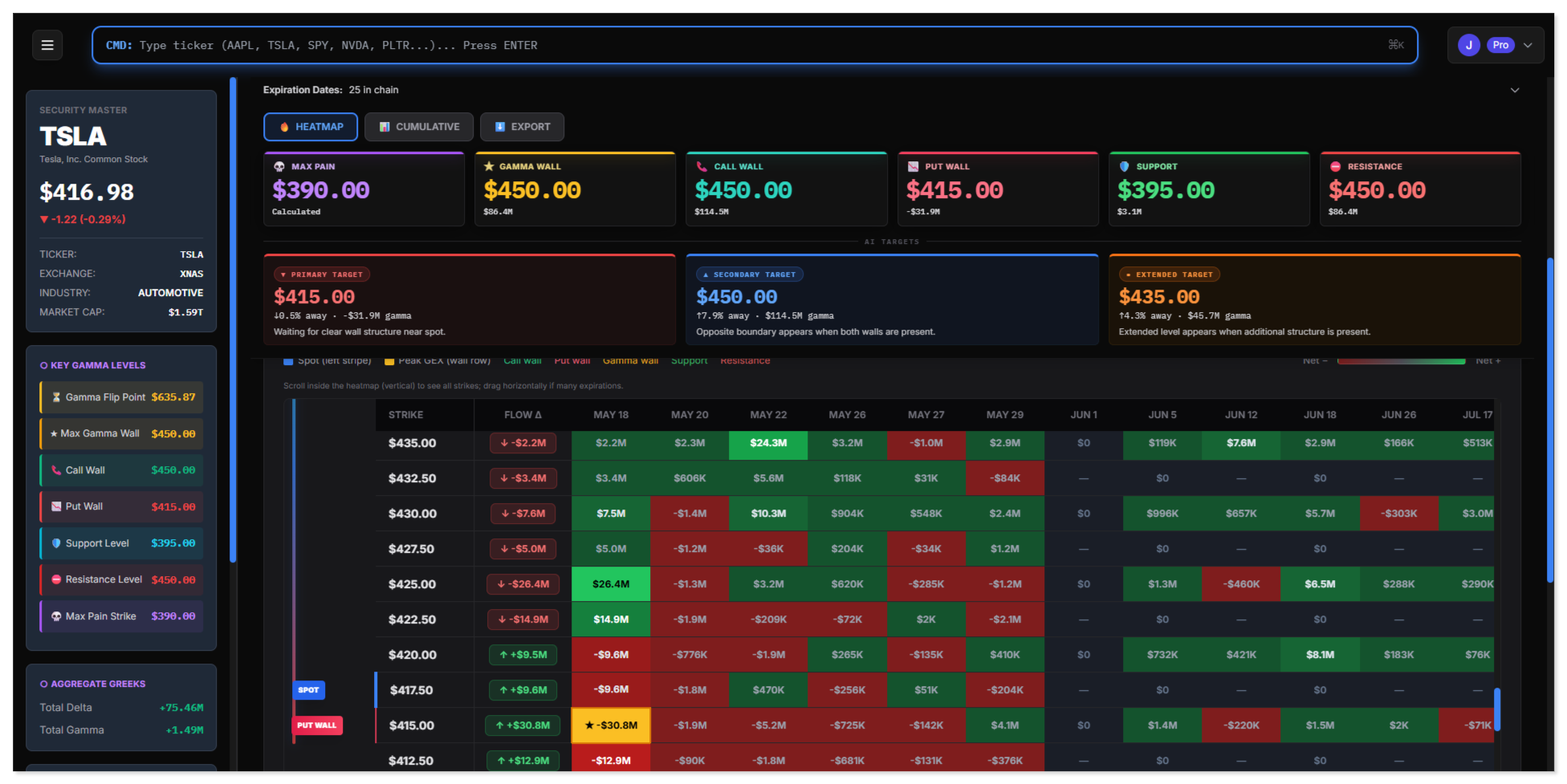

Max Pain: Price Gravity Around Expiration

Max pain is the strike price at which the total value of all open options contracts is minimized – the price where the maximum number of options expire worthless, leaving option buyers with the most losses.

This isn’t manipulation. It’s a natural consequence of dealer hedging. As expiration approaches, market makers reduce their delta hedges on expiring positions. That unwinding mechanically moves price toward the strike with the least aggregate payout – max pain.

How strong is the max pain effect?

It’s real, but not guaranteed. The effect tends to be strongest:

- In the final 2–3 trading days before monthly expiration

- When there’s no major external catalyst overriding the mechanical drift

- When max pain is within a few percent of the current price

When a macro event hits (CPI, Fed decision, earnings from a major name), max pain is often overwhelmed. But in quiet, low-catalyst expiration weeks, it’s a powerful gravitational force.

How to Manage Options Into Expiration

Here’s a practical framework for managing open positions as expiration approaches:

30+ DTE: No action needed unless thesis has changed

This is your cushion zone. Theta decay exists but is manageable. Focus on whether your directional thesis is still valid, not on the calendar.

14–21 DTE: Begin evaluating

If the trade is working (up 50%+), consider taking partial or full profit. You’ve captured most of the move and the time value remaining is shrinking. If the trade is losing, assess whether the thesis is intact or broken. Don’t hold a losing OTM option into this zone hoping for rescue.

7–10 DTE: High attention zone

Theta acceleration is significant. Unless you’re specifically managing a position with a short-term catalyst incoming, start closing losing trades here. The cost of holding a 40% loser from 7 DTE to 0 DTE is usually the remaining 60% – not a recovery.

1–3 DTE: Close or roll

For most beginner trades: close the position and reassess. Don’t hold OTM options through the final days unless you have a very specific reason. The gamma is extreme, the theta is punishing, and the risk/reward has usually deteriorated significantly.

0DTE Options: Expiration as the Trade

0DTE (zero days to expiration) options are contracts that expire the same day they’re traded. These have become enormously popular – on SPX and SPY, 0DTE volume now represents a significant portion of all daily options activity.

The mechanics at 0DTE are extreme:

- Gamma is maximum – small stock moves produce large percentage gains or losses

- Theta decays to zero by close – every extrinsic value dollar disappears by 4pm

- Bid-ask spreads can widen intraday – liquidity drops fast on non-standard expirations

0DTE trading is not a beginner strategy. The leverage is real, but so is the speed of loss. A position can go from +200% to zero in a single 15-minute move. Master the fundamentals and have a risk framework before approaching 0DTE.

Coming soon on SweepAlgo: 0DTE-specific GEX analysis, filtering gamma walls by same-day expiration for intraday traders.

FAQ

When do options expire exactly?

Most equity options expire at market close (4:00 PM ET) on their expiration date. SPX options have a nuance – monthly SPX options (AM-settled) expire at the open on expiration Friday, while weekly SPX options expire at the close. Check which settlement type you’re trading.

What happens if I don’t close my option before expiration?

If it’s in-the-money, your broker will typically auto-exercise it, meaning you’d buy or sell 100 shares at the strike price. If it’s out-of-the-money, it expires worthless. Most retail traders should close before expiration to avoid exercise complications.

Can I lose more than I paid if my option expires in the money?

No. As a buyer of options, your maximum loss is the premium paid. Auto-exercise of an ITM call could require you to fund a stock purchase, but you can avoid this by closing the contract before expiration.

What is options pinning at expiration?

Pinning is when price gravitates toward and stays near a specific strike into expiration – typically the strike with the most open interest (max pain). It’s driven by dealer hedging as they manage expiring books. It’s most common in the final 2–3 days of monthly expiration.

Should beginners trade weekly or monthly options?

Start with monthly options (30–45 DTE). They give you more time for the thesis to play out, have lower theta decay per day, and are more forgiving of imprecise timing. Move to weeklies once you’re comfortable with how theta and expiration mechanics work in practice.

What is the difference between AM and PM settlement for SPX?

Monthly SPX options (standard) are AM-settled – they expire based on the Friday morning open price, not the close. This can cause confusion because the options stop trading Thursday evening but the settlement price isn’t determined until Friday morning. Weekly SPX options are PM-settled (expire at Friday close). Most beginners should use SPY (PM-settled) to avoid AM settlement confusion.

The Bottom Line

Expiration isn’t just an end date – it’s an active force on your position from the moment you buy. Theta accelerates, max pain pulls price, and the structural dynamics of the market shift as open interest in expiring contracts unwinds. Understanding this calendar-driven behavior is what separates traders who make money on correct directional calls from those who are right about direction and still lose money.

See live max pain levels and GEX structure for the current expiration on SweepAlgo →

Disclaimer: This content is for educational purposes only and does not constitute financial advice. Options trading involves substantial risk of loss and is not appropriate for all investors.